diff options

Diffstat (limited to 'content/blog/2020-09-22-internal-audit.md')

| -rw-r--r-- | content/blog/2020-09-22-internal-audit.md | 19 |

1 files changed, 10 insertions, 9 deletions

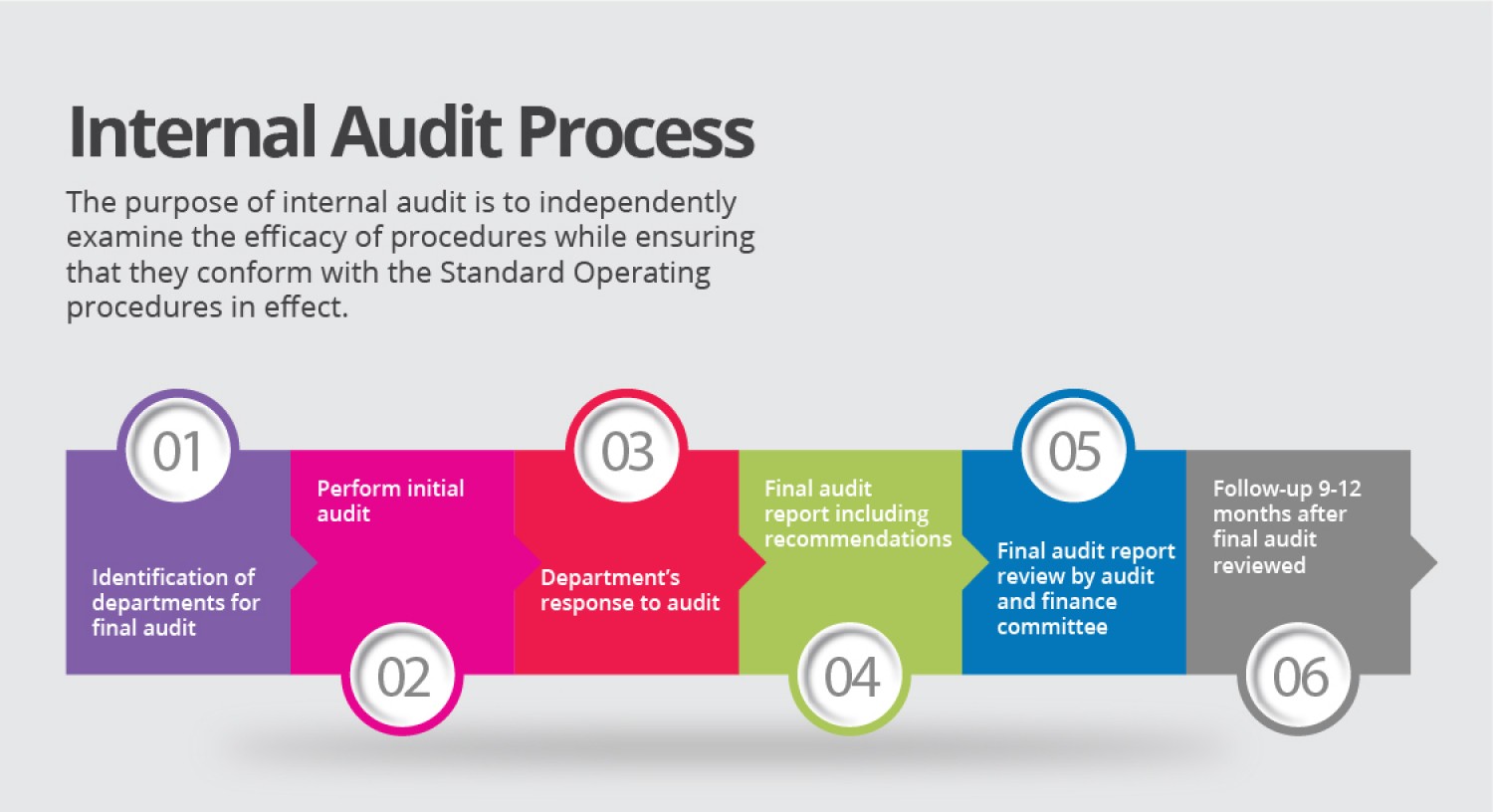

diff --git a/content/blog/2020-09-22-internal-audit.md b/content/blog/2020-09-22-internal-audit.md index 39c1cce..62e8da0 100644 --- a/content/blog/2020-09-22-internal-audit.md +++ b/content/blog/2020-09-22-internal-audit.md @@ -12,8 +12,8 @@ Overview](https://img.cleberg.net/blog/20200922-what-is-internal-audit/internal- One of the many reasons that Internal Audit needs such thorough explaining to non-auditors is that Internal Audit can serve many purposes, depending on the -organization's size and needs. However, the Institute of Internal Auditors -(IIA) defines Internal Auditing as: +organization's size and needs. However, the Institute of Internal Auditors (IIA) +defines Internal Auditing as: > Internal auditing is an independent, objective assurance and consulting > activity designed to add value and improve an organization's operations. It @@ -54,9 +54,10 @@ function, process, system, or other subject matters. The internal auditor determines the nature and scope of an assurance engagement. Generally, three parties are participants in assurance services: (1) the person or group directly involved with the entity, operation, function, process, system, or other subject -- (the process owner), (2) the person or group making the assessment - (the -internal auditor), and (3) the person or group using the assessment - (the -user). + +- (the process owner), (2) the person or group making the assessment - (the + internal auditor), and (3) the person or group using the assessment - (the + user). ## Consulting @@ -121,10 +122,10 @@ model. Looking at this model from an auditing perspective shows us that auditors will need to align, communicate, and collaborate with management, including business area managers and chief officers, as well as reporting to the governing body. -The governing body will instruct internal audit *functionally* on their goals +The governing body will instruct internal audit _functionally_ on their goals and track their progress periodically. -However, the internal audit department will report *administratively* to a chief +However, the internal audit department will report _administratively_ to a chief officer in the company for the purposes of collaboration, direction, and assistance with the business. Note that in most situations, the governing body is the audit committee on the company's board of directors. @@ -136,8 +137,8 @@ objective function that can provide assurance over the topics they audit. A normal audit will generally follow the same process, regardless of the topic. However, certain special projects or abnormal business areas may call for -changes to the audit process. The audit process is not set in stone, it's -simply a set of best practices so that audits can be performed consistently. +changes to the audit process. The audit process is not set in stone, it's simply +a set of best practices so that audits can be performed consistently.  |