diff options

| author | Christian Cleberg <hello@cleberg.net> | 2024-03-04 22:34:28 -0600 |

|---|---|---|

| committer | Christian Cleberg <hello@cleberg.net> | 2024-03-04 22:34:28 -0600 |

| commit | 797a1404213173791a5f4126a77ad383ceb00064 (patch) | |

| tree | fcbb56dc023c1e490df70478e696041c566e58b4 /content/blog/2019-09-09-audit-analytics.md | |

| parent | 3db79e7bb6a34ee94935c22d7f0e18cf227c7813 (diff) | |

| download | cleberg.net-797a1404213173791a5f4126a77ad383ceb00064.tar.gz cleberg.net-797a1404213173791a5f4126a77ad383ceb00064.tar.bz2 cleberg.net-797a1404213173791a5f4126a77ad383ceb00064.zip | |

initial migration to test org-mode

Diffstat (limited to 'content/blog/2019-09-09-audit-analytics.md')

| -rw-r--r-- | content/blog/2019-09-09-audit-analytics.md | 231 |

1 files changed, 0 insertions, 231 deletions

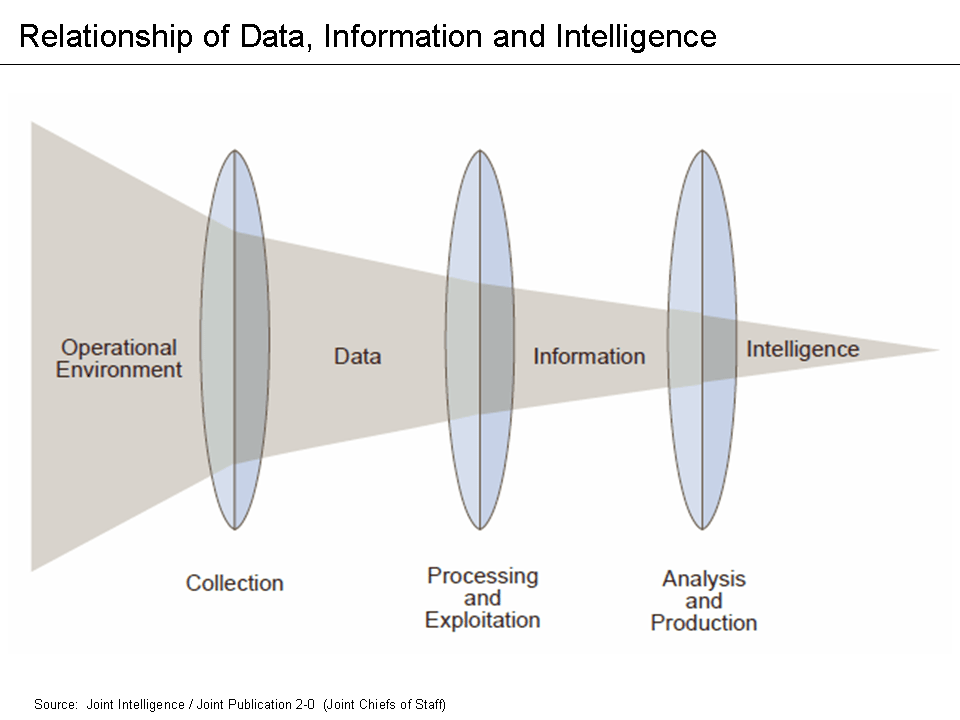

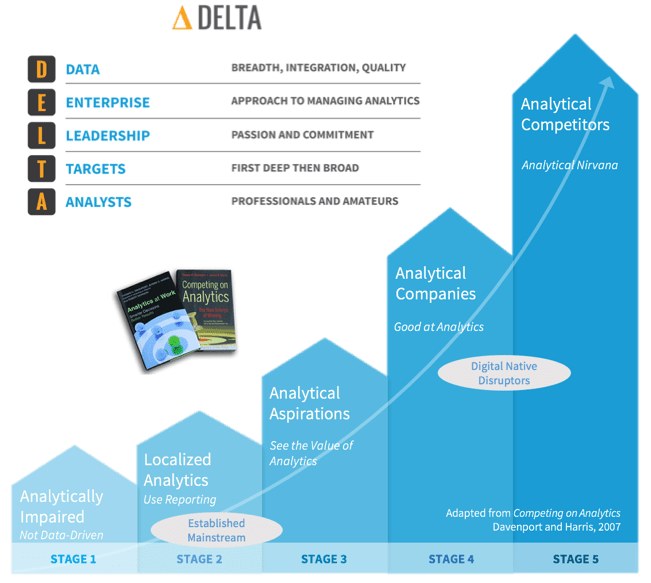

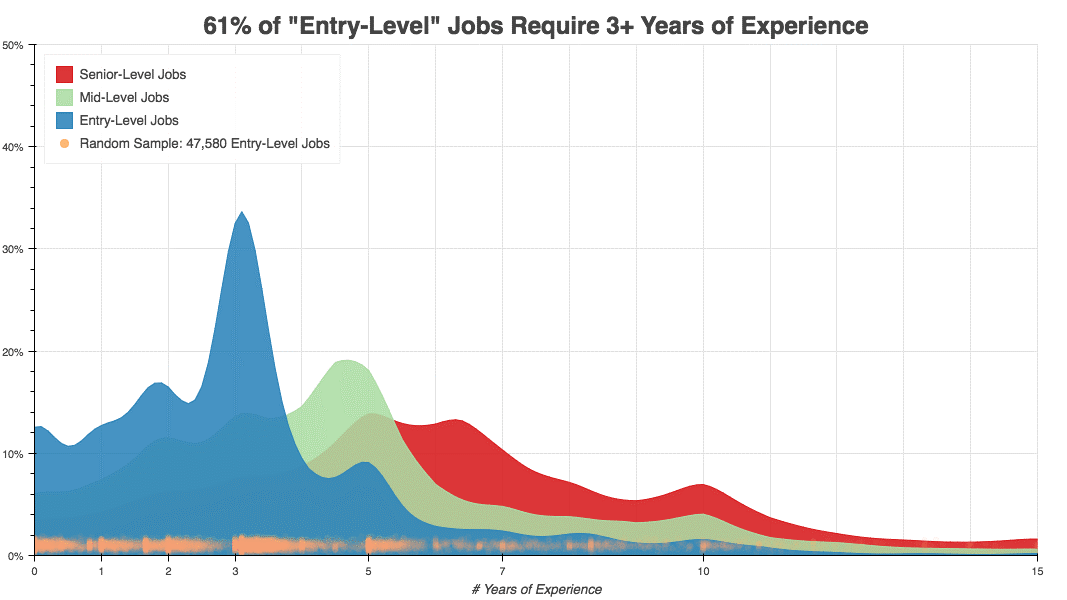

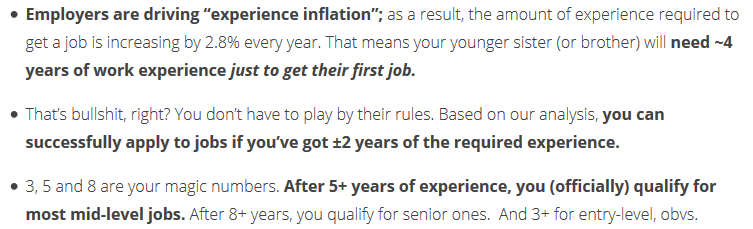

diff --git a/content/blog/2019-09-09-audit-analytics.md b/content/blog/2019-09-09-audit-analytics.md deleted file mode 100644 index 7be3d92..0000000 --- a/content/blog/2019-09-09-audit-analytics.md +++ /dev/null @@ -1,231 +0,0 @@ -+++ -date = 2019-09-09 -title = "Data Analysis in Auditing" -description = "Learn how to use data analysis in the world of auditing." -+++ - -# What Are Data Analytics? - -A quick aside before I dive into this post: `data analytics` is a -vague term that has become popular in recent years. Think of a `data -analytic` as the output of any data analysis you perform. For example, -a pivot table or a pie chart could be a data analytic. - -[Data analysis](https://en.wikipedia.org/wiki/Data_analysis) is a -process that utilizes statistics and other mathematical methods to -discover useful information within datasets. This involves examining, -cleaning, transforming, and modeling data so that you can use the data -to support an opinion, create more useful viewpoints, and gain knowledge -to implement into audit planning or risk assessments. - -One of the common mistakes that managers (and anyone new to the process) -make is assuming that everything involved with this process is "data -analytics". In fact, data analytics are only a small part of the -process. - -See **Figure 1** for a more accurate representation of where data -analysis sits within the full process. This means that data analysis -does not include querying or extracting data, selecting samples, or -performing audit tests. These steps can be necessary for an audit (and -may even be performed by the same associates), but they are not data -analytics. - - - -# Current Use of Analytics in Auditing - -While data analysis has been an integral part of most businesses and -departments for the better part of the last century, only recently have -internal audit functions been adopting this practice. The internal audit -function works exclusively to provide assurance and consulting services -to the business areas within the firm (except for internal auditing -firms who are hired by different companies to perform their roles). - -> Internal Auditing helps an organization accomplish its objectives by -> bringing a systematic, disciplined approach to evaluate and improve -> the effectiveness of risk management, control and governance -> processes. -> -> - The IIA's Definition of Internal Audit - -Part of the blame for the slow adoption of data analysis can be -attributed to the fact that internal auditing is strongly based on -tradition and following the precedents set by previous auditors. -However, there can be no progress without auditors who are willing to -break the mold and test new audit techniques. In fact, as of 2018, [only -63% of internal audit departments currently utilize data -analytics](https://www.cpapracticeadvisor.com/accounting-audit/news/12404086/internal-audit-groups-are-lagging-in-data-analytics) -in North America. This number should be as close as possible to 100%. I -have never been part of an audit that would not have benefited from data -analytics. - -So, how do internal audit functions remedy this situation? It's -definitely not as easy as walking into work on Monday and telling your -Chief Audit Executive that you're going to start implementing analytics -in the next audit. You need a plan and a system to make the analysis -process as effective as possible. - -# The DELTA Model - -One of the easiest ways to experiment with data analytics and gain an -understanding of the processes is to implement them within your own -department. But how do we do this if we've never worked with analysis -before? One of the most common places to start is to research some data -analysis models currently available. For this post, we'll take a look -at the DELTA model. You can take a look at ****Figure 2**** for a quick -overview of the model. - -The DELTA model sets a few guidelines for areas wanting to implement -data analytics so that the results can be as comprehensive as possible: - -- **Data**: Must be clean, accessible, and (usually) unique. -- **Enterprise-Wide Focus**: Key data systems and analytical resources - must be available for use (by the Internal Audit Function). -- **Leaders**: Must promote a data analytics approach and show the - value of analytical results. -- **Targets**: Must be set for key areas and risks that the analytics - can be compared against (KPIs). -- **Analysts**: There must be auditors willing and able to perform - data analytics or else the system cannot be sustained. - - - -# Finding the Proper KPIs - -Once the Internal Audit Function has decided that they want to start -using data analytics internally and have ensured they're properly set -up to do so, they need to figure out what they will be testing against. -Key Performance Indicators (KPIs) are qualitative or quantitative -factors that can be evaluated and assessed to determine if the -department is performing well, usually compared to historical or -industry benchmarks. Once KPIs have been agreed upon and set, auditors -can use data analytics to assess and report on these KPIs. This allows -the person performing the analytics the freedom to express opinions on -the results, whereas the results are ambiguous if no KPIs exist. - -It should be noted that tracking KPIs in the department can help ensure -you have a rigorous Quality Assurance and Improvement Program (QAIP) in -accordance with some applicable standards, such as IPPF Standard 1300. - -> The chief audit executive must develop and maintain a quality assurance -> and improvement program that covers all aspects of the internal audit -> activity. -> -> - IPPF Standard 1300 - -Additionally, IPPF Standard 2060 discusses reporting: - -> The chief audit executive must report periodically to senior -> management and the board on the internal audit activity's purpose, -> authority, responsibility, and performance relative to its plan and on -> its conformance with the Code of Ethics and the Standards. Reporting -> must also include significant risk and control issues, including fraud -> risks, governance issues, and other matters that require the attention -> of senior management and/or the board. -> -> - IPPF Standard 2060 - -The hardest part of finding KPIs is to determine which KPIs are -appropriate for your department. Since every department is different and -has different goals, KPIs will vary drastically between companies. To -give you an idea of where to look, here are some ideas I came up with -when discussing the topic with a few colleagues. - -- Efficiency/Budgeting: - - Audit hours to staff utilization ratio (annual hours divided by - total annual work hours). - - Audit hours compared to the number of audits completed. - - Time between audit steps or to complete the whole audit. E.g., - time from fieldwork completion to audit report issuance. -- Reputation: - - The frequency that management has requested the services of the - IAF. - - Management, audit committee, or external audit satisfaction - survey results. - - Education, experience, certifications, tenure, and training of - the auditors on staff. -- Quality: - - Number and frequency of audit findings. Assign monetary or - numerical values, if possible. - - Percentage of recommendations issued and implemented. -- Planning: - - Percentage or number of key risks audited per year or per audit. - - Proportion of audit universe audited per year. - -# Data Analysis Tools - -Finally, to be able to analyze and report on the data analysis, auditors -need to evaluate the tools at their disposal. There are many options -available, but a few of the most common ones can easily get the job -done. For example, almost every auditor already has access to Microsoft -Excel. Excel is more powerful than most people give it credit for and -can accomplish a lot of basic statistics without much work. If you -don't know a lot about statistics but still want to see some of the -more basic results, Excel is a great option. - -To perform more in-depth statistical analysis or to explore large -datasets that Excel cannot handle, auditors will need to explore other -options. The big three that have had a lot of success in recent years -are Python, R, and ACL. ACL can be used as either a graphical tool -(point and click) or as a scripting tool, where the auditor must write -the scripts manually. Python and the R-language are solely scripting -languages. - -The general trend in the data analytics environment is that if the tool -allows you to do everything by clicking buttons or dragging elements, -you won't be able to fully utilize the analytics you need. The most -robust solutions are created by those who understand how to write the -scripts manually. It should be noted that as the utility of a tool -increases, it usually means that the learning curve for that tool will -also be higher. It will take auditors longer to learn how to utilize -Python, R, or ACL versus learning how to utilize Excel. - -# Visualization - -Once an auditor has finally found the right data, KPIs, and tools, they -must report these results so that actions can be taken. Performing -in-depth data analysis is only useful if the results are understood by -the audiences of the data. The best way to create this understanding is -to visualize the results of the data. Let's take a look at some of the -best options to visualize and report the results you've found. - -Some of the most popular commercial tools for visualization are -Microsoft PowerBI and Tableau Desktop. However, other tools exist such -as JMP, Plotly, Qlikview, Alteryx, or D3. Some require commercial -licenses while others are simply free to use. For corporate data, you -may want to make sure that the tool does not communicate any of the data -outside the company (such as cloud storage). I won't be going into -depth on any of these tools since visualization is largely a subjective -and creative experience, but remember to constantly explore new options -as you repeat the process. - -Lastly, let's take a look at an example of data visualization. This -example comes from a [blog post written by Kushal -Chakrabarti](https://talent.works/2018/03/28/the-science-of-the-job-search-part-iii-61-of-entry-level-jobs-require-3-years-of-experience/) -in 2018 about the percent of entry-level US jobs that require -experience. **Figure 3** shows us an easy-to-digest picture of the data. -We can quickly tell that only about 12.5% of entry-level jobs don't -require experience. - -This is the kind of result that easily describes the data for you. -However, make sure to include an explanation of what the results mean. -Don't let the reader assume what the data means, especially if it -relates to a complex subject. *Tell a story* about the data and why the -results matter. For example, **Figure 4** shows a part of the -explanation the author gives to illustrate his point. - - - - - -# Wrap-Up - -While this is not an all-encompassing program that you can just adopt -into your department, it should be enough to get anyone started on the -process of understanding and implementing data analytics. Always -remember to continue learning and exploring new options as your -processes grow and evolve. |